Journey Optimization • Product StrategyUncovering Friction in RBC Onboarding

Targeted optimizations in self-service and advisor-assisted flows reduced abandonment by 67% at RBC.

Role

Senior Product Designer

Platform

Web

Mobile

Team

Cross-functional (Designers, Developers, Product Managers, Leadership)

Impact

19 percentage points reduction in abandonment (28% → 9%)

20+ user interviews conducted

3 experience types designed and launched

4 journey scenarios mapped and redesigned

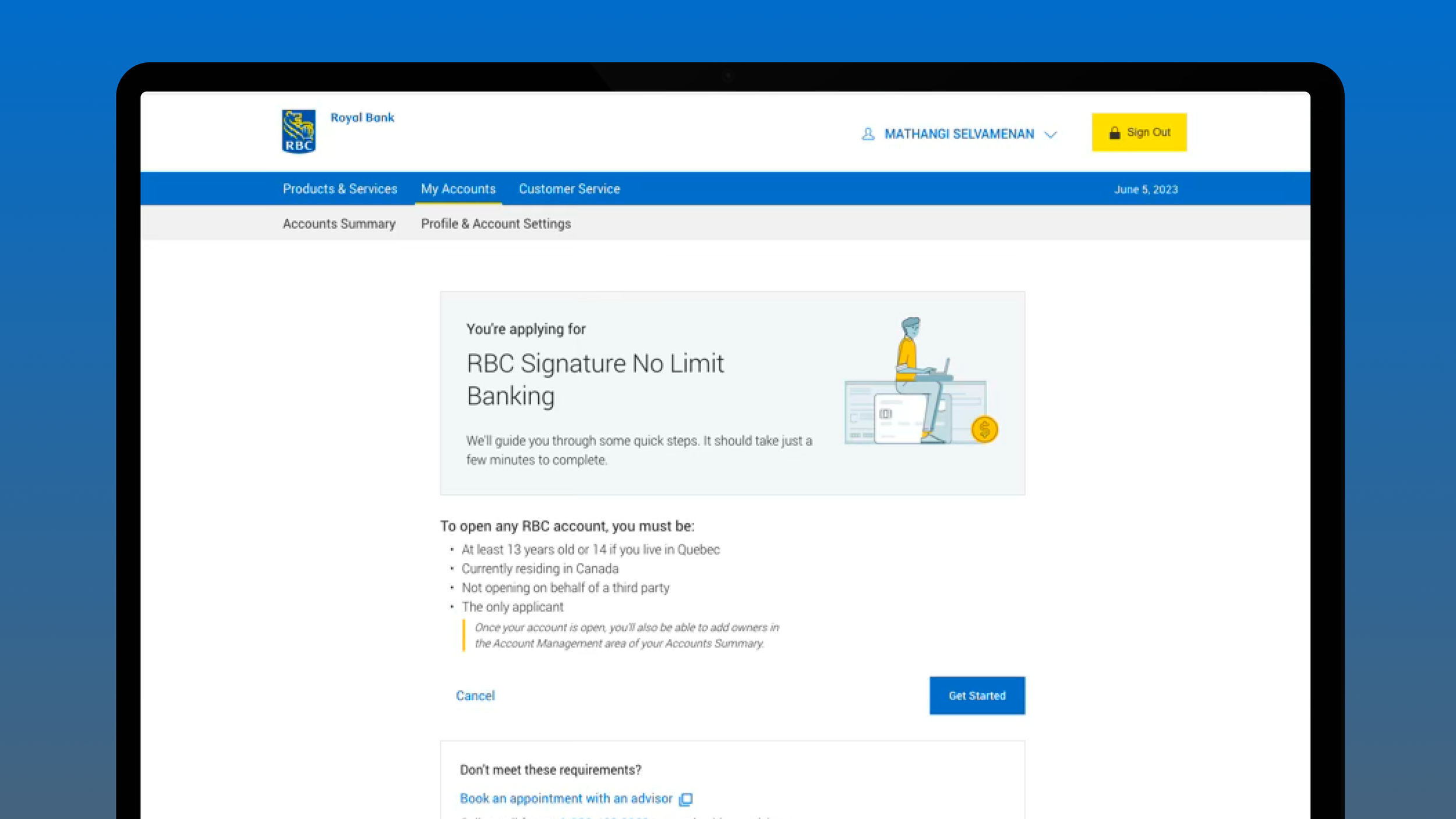

The Problem

RBC's account opening experience was broken. Customers completed the online portion, but 28% never came back to finish in-branch. The process had too many steps, unclear requirements, and disconnected experiences across channels.

The bank recognized customers have different preferences—some want self-service, some want guidance, some want a mix. COVID-19 made solving this problem urgent.

Research

I conducted extensive user research to understand expectations, pain points, and motivations across different customer types. This included interviews, surveys, benchmarking, and usability testing.

Key Findings

Self-service users wanted:

Complete autonomy without needing a banking specialist

Convenient ID verification through mobile

Clear, concise instructions guiding them through the process

Advisor-assisted users wanted:

Personalized guidance and expertise during account opening

Seamless transitions between digital and physical channels

No repeating steps already completed online

In-branch users wanted:

Reduced complexity when meeting with specialists

Smooth collaboration between themselves and advisors

Quick, efficient completion

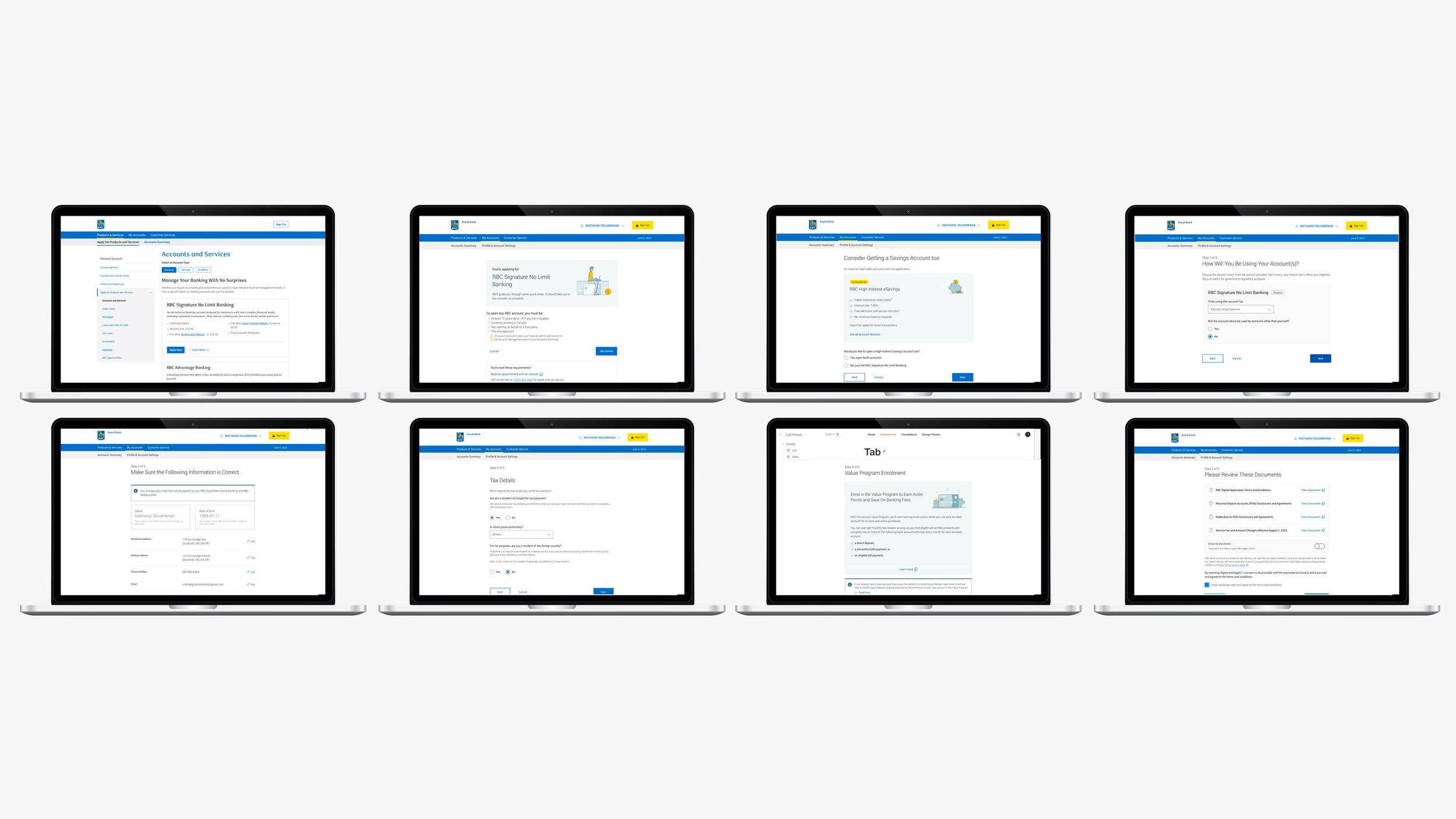

The Solution

We designed three distinct experience types to match customer preferences:

1. Self-Service (Complete Autonomy)

User-guided, fully digital experience with no RBC advisor involvement.

2. Advisor-Assisted (Hybrid, Remote)

Video or phone call with an RBC advisor, combining digital tools with human guidance.

3. In-Branch (Hybrid, Co-Located)

Start online, complete in person with an advisor—seamless handoff, no repeated steps.

Core Journey Flow

Select account type

Add savings account (optional)

View account details

Enter purpose of account

Confirm/enter personal details

Enroll in value programs (optional)

Confirm tax details

eSign documents

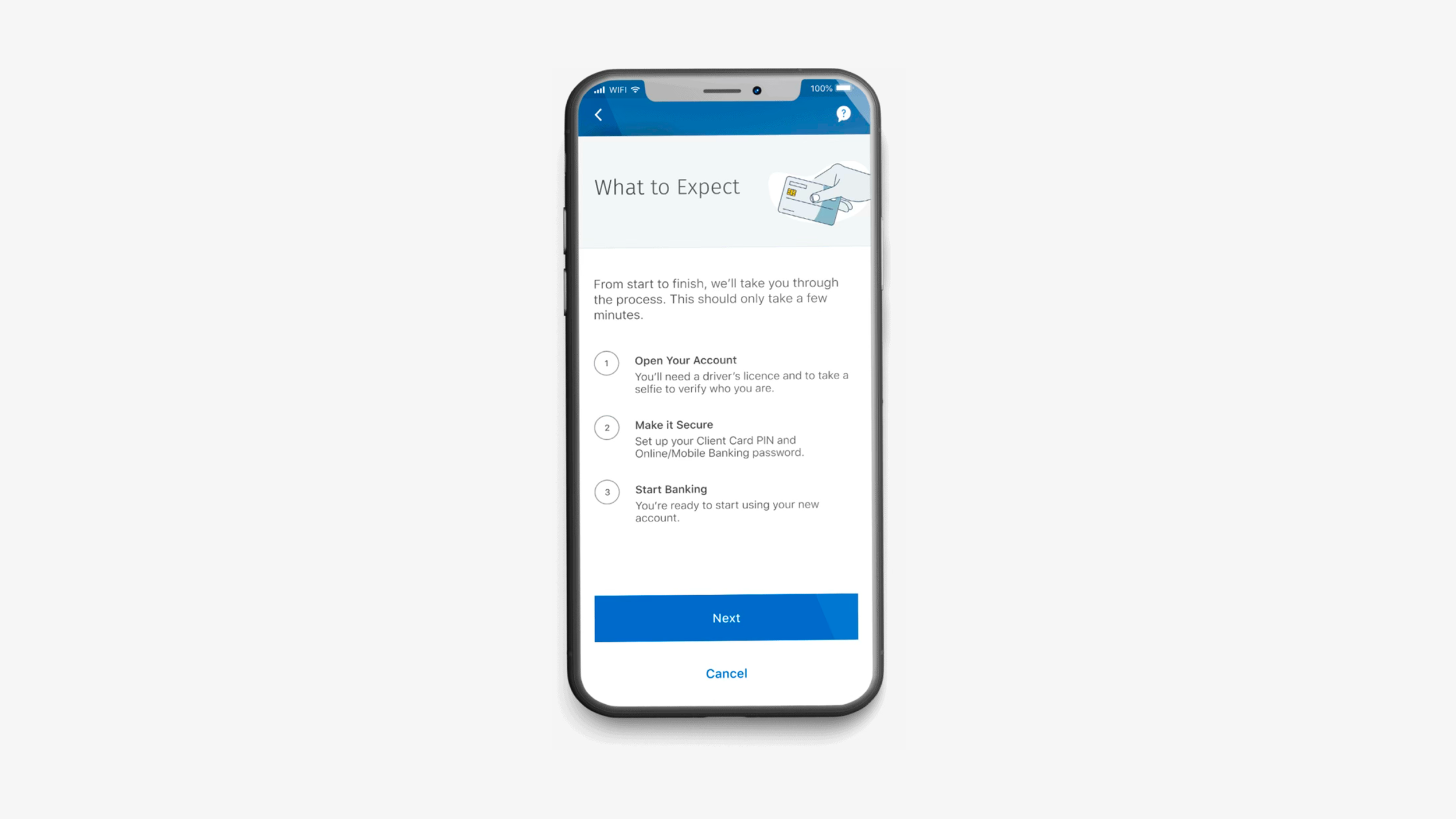

For in-branch experiences, advisors conduct manual ID checks or assist with document verification, creating a collaborative environment that reduces friction.

The Approach

I led the end-to-end redesign—mapping journey scenarios, identifying friction points, and designing solutions using progressive disclosure. Information was requested only when needed. Progress indicators showed customers where they were. Contextual help appeared exactly where people got stuck.

I worked closely with a UX researcher and visual designer throughout discovery, design, and validation. We tested prototypes, gathered feedback, and iterated until the experience felt seamless.

Results

Stale accounts, onboarding abandonment dropped from 28% to 9% (67% reduction)

3 experience types launched to match customer preferences

Increased autonomy for self-service users

Improved efficiency across all channels

Enhanced trust and security through clear communication

Seamless transitions between digital and in-person experiences

Competitive advantage positioning RBC as customer-centric

What I Learned

Progressive disclosure works. Asking for information only when it's needed reduces cognitive load and prevents drop-off at critical moments.

Different customers need different paths. One size doesn't fit all. Designing for choice and flexibility increases satisfaction and conversion.

Seamless handoffs matter. When customers move between channels, they shouldn't repeat themselves. Continuity builds trust and reduces frustration.